I. At a Breaking Point? Four Structural "Truths" We Are Currently Experiencing

If there is one word to describe the titanium and zirconium market in 2025, many industry peers would choose "challenging". Operating on the frontlines of the market, we have identified four ongoing structural shifts:

(I) Resource Anxiety: Persistent Dependency Coupled with High Volatility

China’s import dependency remains stubbornly high, with over 80% of zircon sand and approximately 40% of titanium ore sourced globally. Concurrently, pricing has been on a rollercoaster ride—zircon sand prices surged to $2,000/ton in 2021, only to plummet back to $1,200/ton by 2023.

(Chart1: Zircon Sand Price Trends)

(II) Low-End Internal Competition: The Tug-of-War Between Sulfate and Chloride Processes

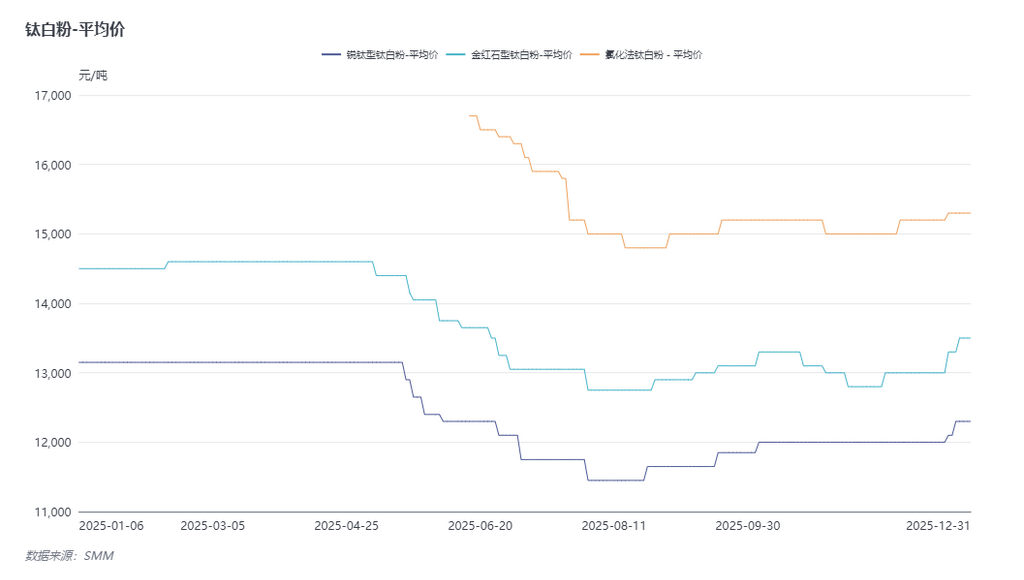

According to data from the Titanium Dioxide Industry Alliance, China’s total titanium dioxide (TiO₂) output in 2025 stood at approximately 3.8 million tons, marking a year-on-year decline of about 2%—the first negative growth recorded in nearly two decades. Within this segment, the sulfate process suffers from severe overcapacity, triggering fierce price wars. Conversely, while the higher-performing chloride process offers superior product quality, its capacity utilization remains constrained due to a critical shortage of high-grade rutile feedstock. This structural mismatch has severely squeezed profit margins across midstream operations.

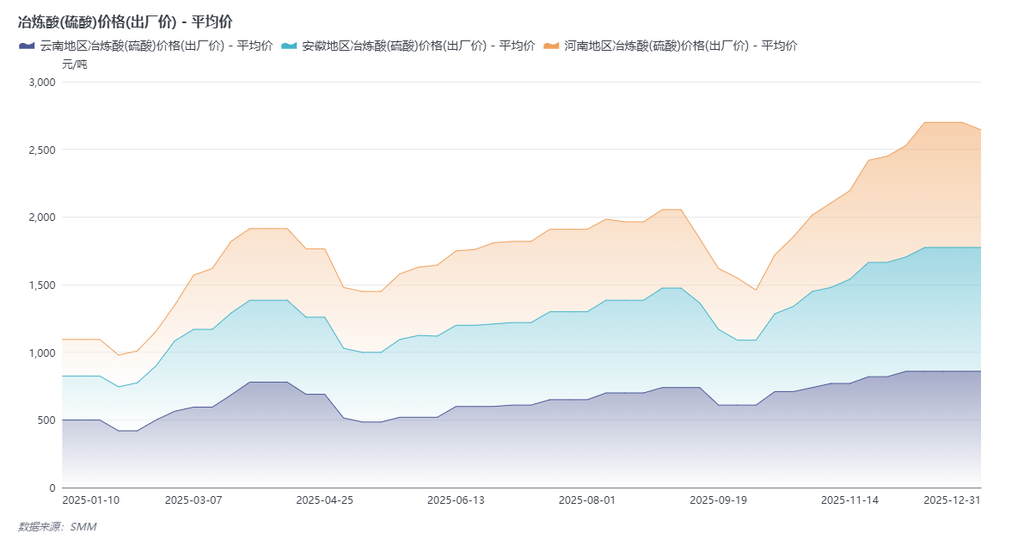

(Chart2: Upward Price Volatility of Sulfuric Acid in 2025)

(Chart3: Price Variance Between Sulfate-Process and Chloride-ProcessTiO)

(III) Application Disconnect: Premium Materials Struggling to Find Immediate Offtake

Taking aerospace-grade titanium alloys as an example, domestic manufacturers are fully capable of producing bars and forgings that meet stringent international standards. However, the qualification cycle for aerospace materials typically spans 3 to 5 years, and extends even further to 5 to 8 years in the nuclear power sector. Consequently, downstream end-users heavily favor certified imported materials, resulting in a frustrating bottleneck where high-quality domestic materials are ready but underutilized.

(IV)Cash Flow Strains: An Unbearable Burden for SMEs

According to widespread industry feedback, the average accounts receivable collection period for small and medium-sized mineral processing plants extended to over 90 days in 2024. A number of these enterprises were forced to suspend operations or exit the market entirely due to liquidity crunches.

II. Shifting Supply-Demand Logic: Penalizing Blind Expansion, Rewarding Precision

The core market dynamic has fundamentally transitioned from "scale-driven competition" to "efficiency and ecosystem-synergy competition".

The Supply Side: Legacy tier-1 mines overseas (such as those in Australia) are entering their depletion phases. Meanwhile, although emerging supply hubs (such as Nigeria) are delivering rapid volume growth, they are plagued by volatile product quality and stringent radiation controls. Pure trading intermediaries who rely solely on arbitrage flipping are seeing their margins evaporate. Today, only raw material suppliers capable of delivering stable, compliant, and customized feedstocks can secure a preferred seat at the table with manufacturers.

The Demand Side: While demand from traditional sectors like construction and ceramics remains sluggish, new growth drivers are rapidly emerging:

The Consumerization of Titanium: E-commerce data from JD.com indicates that the compound annual growth rate (CAGR) of titanium cookware transaction volumes reached 109% from 2023 to 2025. Additionally, institutional research reports show that cumulative consumption of titanium raw materials in the consumer electronics sector exceeded 15,000 tons between 2024 and 2025.

High-End Shifts in Zirconium: Prices have remained highly resilient for high-purity zirconia (4N grade and above) used in solid-state battery electrolytes, as well as zirconium powder utilized in 5G ceramic filters.

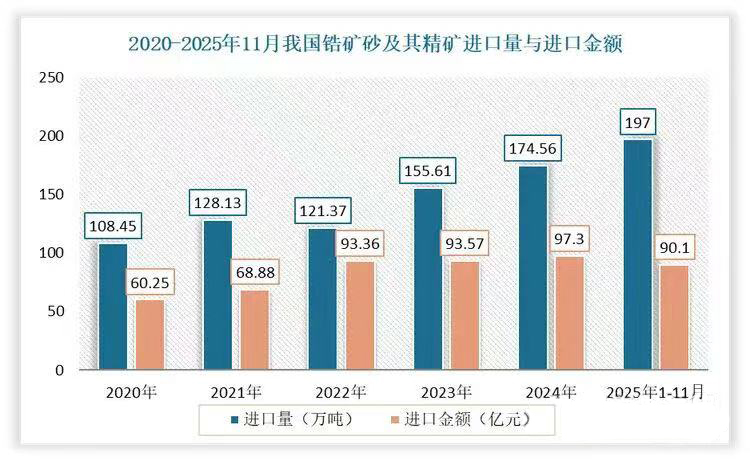

(Chart4: Year-on-Year Growth in Imports of Zircon Ore and Concentrates; Data Sources: General Administration of Customs, Ganyan Report)

III. Value Reconfiguration: Serving as the "Coupling Agent" for the Supply Chain

With demand and supply both in flux, who will bridge the systemic gap in between? No single miner or manufacturer can weather these cyclical macro shifts alone. We prefer to collaborate with our partners to transform individual resources, distribution channels, and institutional credit into a shared "coupling agent"—which is precisely where our long-term value lies.

(I)Bespoke, Tailored Solutions

Our approach begins by understanding our clients' specific application requirements. For partners producing chloride-processTiO, we actively optimize and control impurity levels such as phosphorus and sulfur. For those producing sponge titanium, we meticulously select rutile feedstocks with specific trace element profiles. Moving away from generic commodities, we focus exclusively on delivering tailored, high-value solutions.

(II) Exercising SOE Credit as an "Anchor of Stability"

Amid intense market volatility, enterprises backed by State-Owned Enterprise (SOE) credit consistently demonstrate superior contract performance and reliability. For instance, during the sharp downturn in TiO₂ prices in August 2025, we honored our original contractual pricing to complete our annual procurement targets, serving as a vital trust stabilizer for both upstream and downstream partners.

(III) Connecting SMEs to the Global Supply Chain

To address the dual bottlenecks of "sourcing constraints and delayed collections," we leverage our established international resource network and a domestic channel capacity capable of absorbing over 200,000 tons of concentrate annually. By introducing flexible supply chain services—such as the proxy-sourcing of premium overseas mineral assets and inventory distribution—we streamline both information and capital flows, enabling supply chain nodes to focus entirely on their core competencies.

IV. Outlook: Where Do We Go From Here?

Looking ahead, the macro trends for the industry are well-defined:

(I)Titanium: Migration from Military to Civil, and Premium to Mass Markets

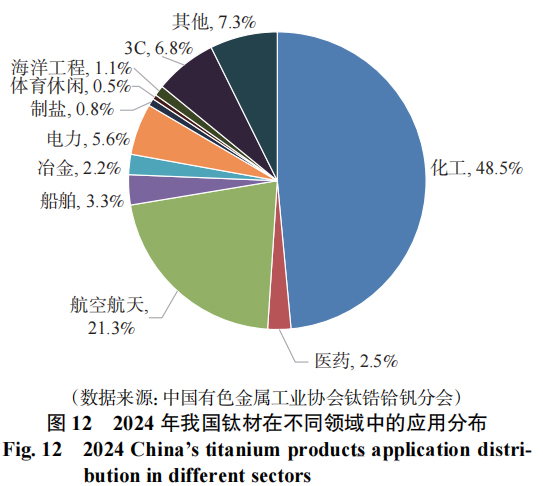

Consumer electronics (such as smartphone frames and smartwatches) have emerged as the largest growth market for titanium, placing exceptionally high demands on material purity. Following Apple’s introduction of a titanium alloy chassis in the iPhone 15 Pro, brands like Huawei, Samsung, and Xiaomi have accelerated adoption, while expanding applications into foldable smartphone hinges and smartwatches. However, transferring aerospace-grade titanium to mass-market commercial applications still requires overcoming steep cost barriers and rigorous qualification thresholds.

(Chart5: Titanium Consumption in the 3C Sector Ranks Third, Trailing Only Chemicals and Aerospace)

(II) Zirconium: An Impending Value Revaluation

The domestic substitution of nuclear-grade zirconium materials has been successfully achieved. The next frontier lies in "energy-grade zirconium". As the commercialization of solid-state batteries accelerates, zirconium is transcending its traditional role as a ceramic raw material to become strategically repositioned as a critical new energy metal.

Behind every ton of mineral sand lies the risk-taking of explorers, the hard labor of miners, and the rigorous craftsmanship of manufacturers. Rather than acting as a detached trading intermediary, we aim to serve as the "industrial adhesive" that binds this supply chain together. Whether you are a titanium manufacturer or a mineral processing plant, if you are experiencing bottlenecks in sourcing, liquidity, or market access, we welcome the opportunity to explore collaborative solutions.

(Note: Certain data and insights in this report are cited from public disclosures by the General Administration of Customs, Northern Nonferrous Metals, SMM, the Titanium, Zirconium, Hafnium and Vanadium Branch of the China Nonferrous Metals Industry Association, and Ganyan Report.)

About the Author

Guangzhou Chemicals Import & Export Co., Ltd., established in 1976, possesses decades of deep-rooted expertise in the zirconium, titanium, daily-use chemical, and industrial chemical feedstock sectors. Backed by robust SOE credit and an extensive global distribution network, the company provides comprehensive, one-stop supply chain solutions spanning raw material imports, product export compliance, and supply chain trade finance.